Playing this video requires a marketing consent.

Click anywhere on the video to renew your consents.

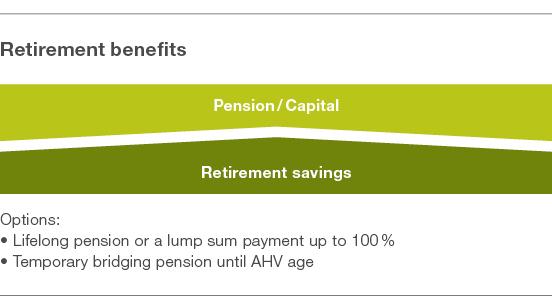

Retirement: pension or lump sum - or both?

Retirement savings can be paid out on retirement either in full or in part as a lump sum or as a lifelong pension.

Ordinary retirement age in the Syngenta Pension Fund at present is 65 for men and women. Early retirement is possible from the age of 60. On retirement, the retirement savings may be converted into a pension and taken in whole or in part as a lump sum.

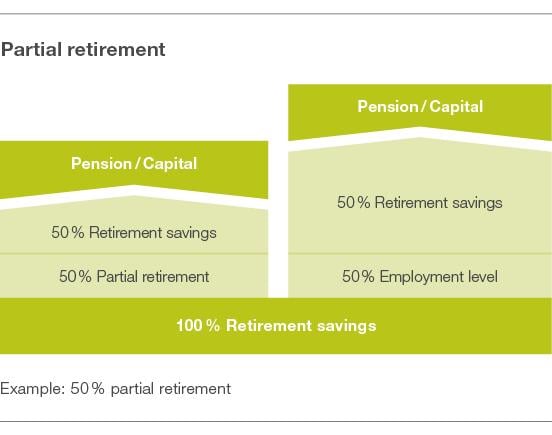

Retirement can be taken in one or more steps (partial retirement).

FAQ

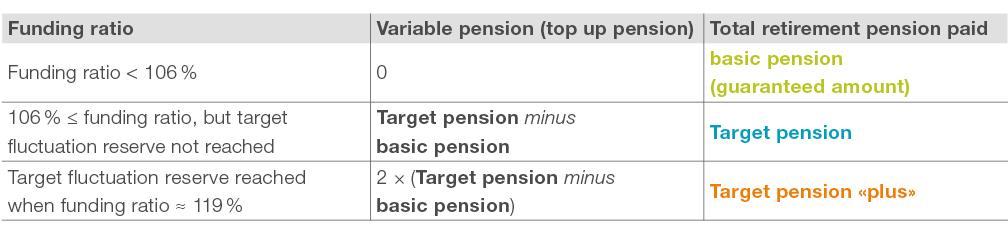

How is the level of the variable retirement pension calculated?

The retirement savings accumulated at the time of retirement are converted into a retirement pension using the conversion rate. The Syngenta retirement pension consists of a basic retirement pension and the variable retirement pension. The guaranteed basic pension is determined on the basis of the conversion rate determining the basic pension. In addition, the target pension is determined on the basis of the conversion rate for determining the target pension.

How is the variable pension determined?

The variable pension is determined annually according to the following scheme, depending on the funding ratio as well as the basic and target retirement pensions calculated at the time of retirement:

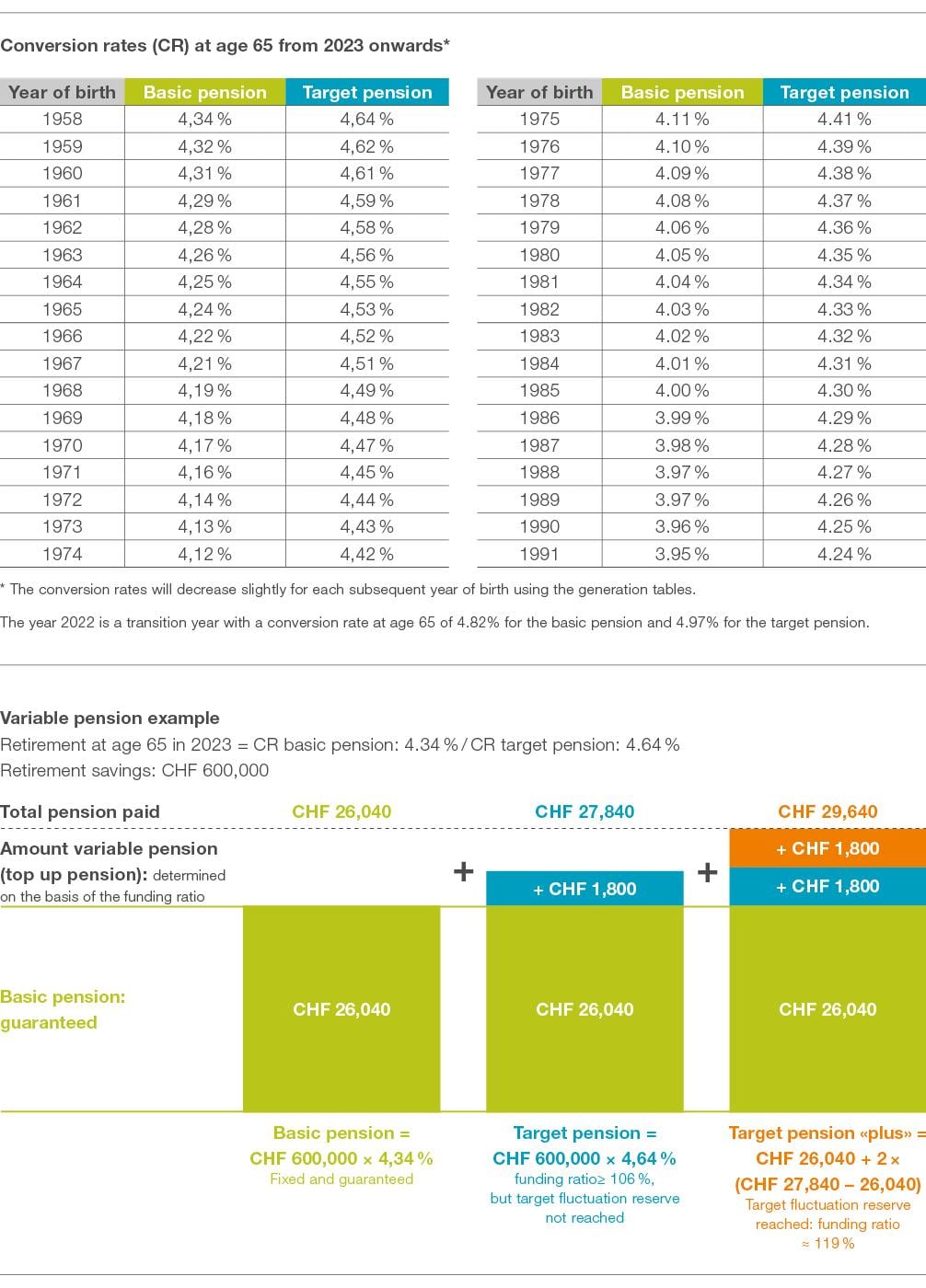

Example calculation of a retirement pension (in CHF) Existing retirement savings: CHF 600 000 Conversion rate (CR): 4.34% Annual retirement pension: CHF 600 000 x 4.34% = 26,040

What conversion rates apply?

The conversion rate is based on the age at the time of retirement. The table below shows the conversion rats at age 65 from 2023 onwards.

Is it possible to pay extra contributions to make up for a reduced pension?

If you retire before the age of 65, it is possible to pay extra contributions to make up for the reduction in pension resulting from early retirement.

What are the conditions for a partial retirement?

In the case of partial retirement, the employment contract must be reduced by at least 30 percent. Partial retirement is only possible with the agreement of the employer.

What benefits do I receive in the case of partial retirement?

The retirement savings are split in line with the reduction in the level of employment. The capital selected for the partial retirement may be converted into a pension. It is also possible to take it wholly or in part as a lump sum.

When does a lump-sum option have to be registered?

The Pension Fund must be notified of the decision to opt for a lump sum payment three months before retirement at the latest.

Why is the spouse’s signature needed in the case of a lump-sum payment?

If a lump sum is taken, the co-insured pension of the spouse is also reduced with the retirement pension.

More information

Download the file 'Regulations of Syngenta Pension Fund' and refer to 'Flexible retirement, Art. 11'

Explanation of terms EN - Conversion rate, Bridging pension, OASI, Retirement child pension

Conversion rate: This percentage is used to convert the retirement savings into a lifelong pension on retirement.

Bridging pension: This temporary pension is paid out until the statutory retirement age for the state pension is reached. You are free to select the level of bridging pension up to an amount equal to the maximum state pension.

OASI: Old-Age and Survivors’ Insurance (the state pension scheme).

Retirement child pension: If the insured member has children aged less than 20 years (or 25 years if they are still in education) a pension equal to 20 percent of the ongoing retirement pension is additionally paid out for each child.